This blog has been written to help our readers understand how TCG can be effectively applied to mobile money assurance activities.

The latest statistics published by the GSMA* state that currently ‘1.75 billion registered accounts are processing $1.4 trillion a year…’. These impressive figures will no doubt continue as the mobile money industry continues to innovate and develop strategic partnerships to provide adjacent services (e.g. credit, savings and insurance). Including the increase of non-mobile network operator services emerging that can compete with the mobile operator services (thereby removing the MNO monopoly).

One of the standout observations was that regulatory changes in-country are having a powerful, controlling influence on mobile money popularity and revenues. By adjusting taxation, or levies, it can either encourage or discourage usage. Restrictions also vary from one country to another, with some allowing and some denying international remittance payments.

The growth of mobile money also has the attention of global financial services, as shown by banks and even Mastercard buying stakes in mobile money services in certain parts of the world.

Other impressive recent mobile money innovations include:

- The rollout of potentially lifesaving insurance services e.g. hospital insurance

- Other types of insurance that might be taken for granted in the Western world e.g. funeral insurance

- Standing orders and debit cards launched in Kenya for mobile money accounts

- The launch of new mobile apps which make mobile money even easier for users

Changes that cause challenges:

- Upgrading or changing mobile money platforms

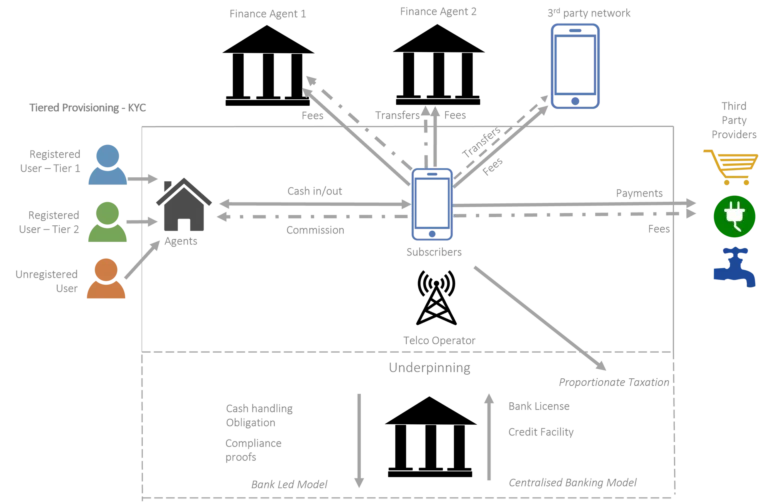

- Revised governmental or banking regulations may require that mobile money service providers need to update their systems, ID verification processes and/or KYC limits

- New mobile money apps launched now have the complexity of integrating with the existing USSD platform

What should be being done?

The GSMA’s code of conduct** highlights what mobile money providers should be doing. From the outset ‘consistent risk mitigation practices’ are highlighted as one way to improve. It continues by saying that the following high-level areas should be considered:

- Improving quality of services and customer satisfaction;

- Facilitating the implementation of trusted partnerships; and

- Building trust with regulators and encouraging the implementation of appropriate and proportional regulatory standards.

To verify compliance, we recommend the use of TCG testing. Shown below are just some of the automated test services that TCG can offer for mobile money as part of a technical risk assessment:

- KYC balance limit verification

- KYC transfer limit verification

- QOS SLA verification and monitoring

- Network availability

- Transfer latency

- Platform message accuracy

- Mobile money account activation/creation (using unregistered SIMs)

- Registered/Unregistered SIM limit testing

- Lost transfers (and lost CDRs)

- Refund verification of expired vouchers

- PIN change limits and rule verification

- USSD platform testing

Our mobile money clients have stressed to us the importance of validating the application of the KYC limits and rules. Particularly when changes are introduced and compliance needs to be immediate to meet governmental or banking requirements.

If you are looking to improve your platforms conduct via risk-mitigation, why not consider how TCG could be used to carry out a technical risk assessment of your mobile money services…

To learn more about our mobile money solutions offered please visit our mobile money independent testing page here.

*Reference: The State of the Industry Report on Mobile Money 2024: https://www.gsma.com/sotir/wp-content/uploads/2024/03/GSMA-SOTIR-2024_Report.pdf

**Reference: GSMA Code of Conduct for Mobile Money Providers: https://www.gsma.com/solutions-and-impact/connectivity-for-good/mobile-for-development/gsma_resources/code-of-conduct-mobile-money-providers/